The hungry grid

Horizon #11: AI is breaking the energy system it needs to survive

Hello everyone. 🌞

A few weeks ago, in the last edition of Horizon, I asked who really controls intelligence in the AI era. The answer, if you remember, wasn’t the labs building the models. It was whoever controls the infrastructure beneath them: compute, capital, and energy.

That last word stayed with me. Energy. I mentioned it as a constraint, but didn’t fully pull on that thread.

This edition does exactly that. Because the more you look at it, the more you realise that the battle for AI isn’t just being fought in data centers and chip fabs. It’s being fought on power grids, in Arctic fjords, and in a decade-long strategic bet made by Beijing that most of the world is only now beginning to understand.

Before we begin, if you’re not yet subscribed, here’s where to do it 👇

You can also follow me and get in touch on my personal media:

Linkedin · X · ipotolot@gmail.com

Earlier this year, Alphabet issued a 100-year bond. The instrument is typically associated with sovereign states, railways, and hydroelectric dams, the kind of obligation you take on when you are not building a product but laying down infrastructure for generations. A company once synonymous with weightless, asset-light technology is now financing itself like an industrial utility from the previous century.

The hunger

Global data center electricity consumption reached approximately 415 TWh in 2024, roughly 1.5% of all electricity consumed on earth, and has been growing at 12% per year for the past five years. The IEA projects it will double by 2030.

Those aggregate figures, however, obscure the sharpness of the local shock. Ireland illustrates the problem with particular clarity. Data centers now account for 22% of Ireland’s total metered electricity consumption, more than every urban household in the country combined. The grid operator placed a moratorium on new data center connections in the Dublin region and, according to EirGrid, that share is expected to rise to 31% by 2034. A small island economy, increasingly shaped by the infrastructure requirements of a handful of multinational hyperscalers.

The same pressure is spreading across traditional European hubs. Amsterdam has paused new projects. Frankfurt is straining. London faces mounting grid constraints. And yet the narrative of scarcity has not stopped investment from flowing. Mistral recently raised $830 million in debt to build a data center south of Paris, having announced in February a separate 1.2-billion-euro plan to build compute capacity in Sweden. The demand is real. The constraint is also real.

The real bottleneck is not technical. Capital moves at the speed of a board decision: a hyperscaler can commit ten billion dollars and break ground within months. Power infrastructure moves at the speed of politics, permits, and physics. Transmission upgrades take years of regulatory approvals, grid interconnections require cross-border negotiations, and no amount of investor enthusiasm can accelerate the physical process of building generation capacity. Electricity supply cannot be conjured by a press release

According to Sightline Climate, up to 50% of announced data center projects could be delayed, with power access as the primary bottleneck. Of 190 gigawatts of tracked capacity, only 5 gigawatts are currently under construction.

Ember estimates that data centers’ share of European electricity demand will grow from 3% today to 5.7% by 2035, with that incremental demand larger than the growth coming from electric vehicles over the same period.

The grid was not built for this.

The paradox

The same technology devouring the grid is also becoming indispensable for running it.

For decades, energy operated on simple logic: centralized generation, passive consumption, manual optimization. Businesses were endpoints in someone else’s infrastructure. The most sophisticated thing a company could do with its energy was negotiate a better rate.

That assumption is now structurally obsolete.

Jonas Janssen, a technology investor, articulated the shift clearly: AI is transforming energy from a static commodity into a programmable, networked system. The conceptual shift is from “what’s our rate?” to “how do we capitalize on volatility?”

Here is why that matters. Every time you run an AI query, train a model, or process data at scale, it consumes electricity. Data centers are being built worldwide to handle this demand, and they are straining power grids that were never designed for this kind of concentrated, continuous load. In that sense, AI is a problem for energy.

But modern grids are also becoming too complex to manage without AI. As more renewable sources come online, wind, solar, distributed storage, the system grows harder to balance in real time. Supply fluctuates with weather. Demand spikes unpredictably. Coordinating thousands of sources and millions of users simultaneously is beyond what human operators and legacy software can handle. In that sense, AI is the solution for energy.

The deeper twist is that the two dynamics reinforce each other. The more AI grows, the more energy it needs, which adds complexity to the grid, which requires more AI to manage. And the smarter the grid becomes through AI, the more efficiently it can power the AI that depends on it. Each new connected asset, a battery, a solar farm, an EV fleet, adds data and control to the system. As Janssen puts it, a single battery is a cost line. Ten thousand batteries orchestrated by AI become a market actor.

AI is both breaking the energy system and building the tools to fix it.

The investment wave

The tension between AI’s hunger and the grid’s limits is creating what may be the most significant investment opportunity of the decade, and it has almost nothing to do with models, benchmarks, or foundation labs.

A recent analysis put it directly: the smartest AI investment right now might be in energy, not in the companies building intelligence but in the companies building the physical substrate that intelligence requires to function.

Three layers of opportunity are emerging simultaneously.

The first is grid modernization. Most of the US grid was built between the 1950s and 1970s. Transmission infrastructure designed for predictable, centralized generation is now absorbing variable renewable inputs from hundreds of thousands of distributed sources while simultaneously handling demand surges from hyperscale AI clusters. Companies like Gridware, Rhizome, and Heimdall Power, a Norwegian startup that helps utilities increase the utilization of existing power lines through software, represent a new category: infrastructure intelligence.

The second layer is storage and flexible demand. Google’s recent deal to power a Minnesota data center using a 30 gigawatt-hour battery from Form Energy points toward the infrastructure required for a genuinely renewable AI grid. A 100-hour storage system that can carry renewable energy across days, not just hours, is beginning to look less like an experiment and more like standard data center equipment.

The third layer is the most structural. Hyperscalers are quietly becoming energy companies. Amazon, Google, Microsoft, and Meta are collectively deploying over $650 billion in capital expenditure, with the majority directed at AI-related infrastructure. They are not waiting for utilities to solve the problem. They are building their own power base.

The Electrostate

To understand where this is heading geopolitically, you need to understand what China has been building for the past decade.

When Xi Jinping took over leadership of the Chinese Communist Party in late 2012, he identified what he called a national security vulnerability. China had become the world’s second-largest economy but remained deeply dependent on imported fossil fuels. Oil and coal imports had surged to record highs, exposing a 1.4 billion person economy to supply disruptions through chokepoints in the Taiwan Strait, the South China Sea, and the Strait of Malacca.

His first direct order to revolutionise China’s energy system came in mid-2014. He told party leaders the energy system suffered from “technological backwardness” and that the country must transform it root and branch.

What followed was a decade of systematic, state-directed investment with few parallels in modern economic history.

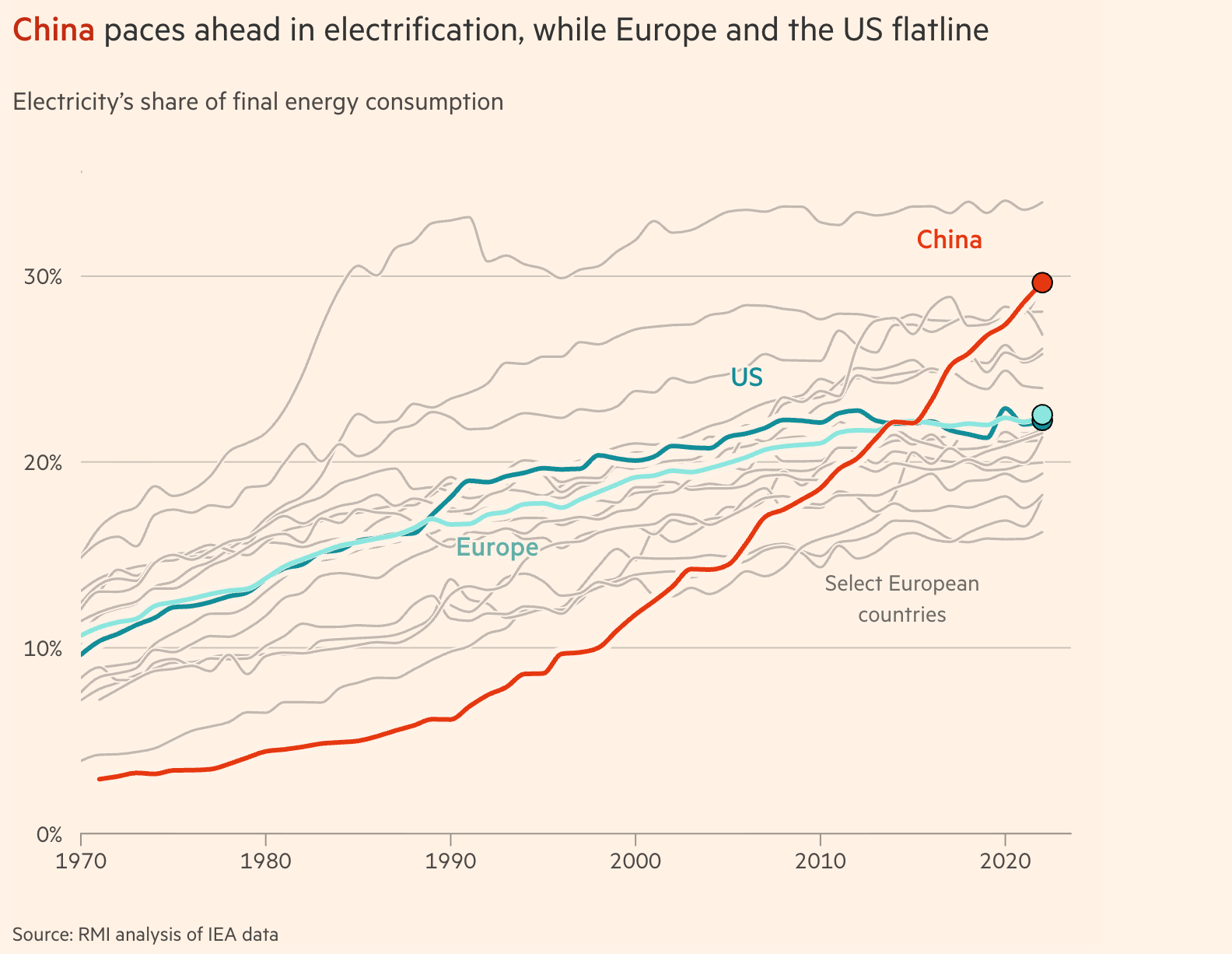

China spent $800 billion in 2025 alone on energy transition investment, roughly 35% of total global spending of $2.3 trillion. It has built more than 40 ultra-high-voltage transmission lines capable of carrying renewable electricity from western deserts to eastern factory hubs. Clean energy sectors accounted for a record 10% of China’s GDP and drove a quarter of its growth last year.

The results are structural. China’s electrification rate has surged to 30%, while Europe and the United States have plateaued at around 22%. China met its 2030 target of 1,200 gigawatts of renewable capacity five years early. It is on course to source 50% of its power from low-carbon sources by 2028.

The Financial Times coined the term that best captures this transformation: China is becoming the world’s first “electrostate.” Just as petrostates built their strategic power on oil and gas, China is constructing a new form of geopolitical leverage built on clean electricity, its manufacturing supply chains, and its control over the critical minerals that underpin the energy transition.

But the most consequential dimension for the AI story is not the renewable deployment alone. It is what China is doing with programmable electricity as a strategic instrument, both domestically and as an export.

On the domestic side, China uses electricity pricing as a precision instrument to shape its industrial structure. Low-tech, high-consumption industries face higher rates, nudging them toward efficiency or exit. Strategic sectors get preferential pricing. AI data centers receive subsidies cutting power bills by up to half, on one condition: they must use locally-made Chinese chips. The grid is not neutral infrastructure. It is a tool for deciding which industries Beijing wants to win.

The export dimension is equally significant, and less discussed. According to the FT, Chinese companies have committed $156 billion in outbound foreign direct investment across more than 200 clean technology transactions since 2023. Nicolas Colin, drawing on this in his late-cycle investment thesis, describes China as offering countries something like a franchise model: not just selling solar panels and wind turbines, but enabling other nations to build their own energy sovereignty on Chinese technology and financing. Countries that adopt this path reduce their dependence on fossil fuel imports, strengthen their own energy security, and, in doing so, deepen their economic relationship with Beijing.

The geopolitical logic is clear. Where petrostates created dependency through fossil fuel exports, the electrostate creates dependency through clean technology exports. The commodity changes; the strategic structure does not. As Tim Buckley of Climate Energy Finance put it to the FT, China is “very well positioned” to emerge from the current geopolitical turbulence with a durable trade weapon: collaboration with any country that wants to pursue energy security and decarbonisation simultaneously.

Beijing has also released a national plan to integrate AI into its energy sector, targeting deployment of at least five industry-specific AI models across power grids, oil, gas, and coal by 2027. The stated goal is to reach globally leading capability in AI energy applications by 2030.

Europe’s unexpected hand

The standard narrative about Europe and AI focuses on its structural lag relative to the United States. No dominant hyperscaler. No frontier model to match the leading American labs at scale, though Mistral is moving fast and investing accordingly. While the US built the intelligence infrastructure and China built the manufacturing base, Europe has been slower to establish its position.

That narrative, however, misses something important happening right now in a town of 21,000 people in the Arctic.

In July 2025, OpenAI announced that its first European data center would not be in London, Frankfurt, or Paris. It would be in Narvik, Norway, a remote industrial town chosen specifically for its surplus of cheap hydroelectric power, cool climate, and low local electricity demand. Sam Altman’s words at the announcement were unambiguous: “I’ve always said we’d love to bring Stargate to Europe if the conditions are right, and we think we’ve found that in Narvik with clean, affordable energy.”

Stargate Norway, a $1 billion joint venture between Nscale, Aker, and OpenAI, will deploy 100,000 NVIDIA GPUs at 230 megawatts of capacity, powered entirely by renewable hydropower, with expansion potential to 520 megawatts. The excess heat from the GPU clusters will be redirected into district heating for local communities, an integration that feels distinctly Nordic in its logic.

It is not an isolated signal. Microsoft, CoreWeave, and Brookfield collectively committed over $15 billion to Nordic AI infrastructure in 2025 alone. Mistral announced its Swedish infrastructure investment of 1.2 billion euros in February. Sweden’s levelized wind power cost fell to $0.03 per kilowatt-hour in 2024, making a 100-megawatt AI cluster in Stockholm meaningfully cheaper to run annually than the equivalent in Frankfurt. OpenAI bypassed the five traditional European data center hubs entirely, because Narvik offered something those cities cannot: abundant, clean, affordable power with room to grow.

What the Nordics have built over decades, through consistent energy policy, cross-border interconnectors, and long-term infrastructure investment, is precisely the asset that AI infrastructure now requires above all others. Norway runs on over 90% hydroelectric generation. Finland generates more than 90% of its electricity from carbon-neutral sources. The Nordic grid is over 90% renewable, stable, and 40-60% cheaper than Western European averages.

These countries did not plan to become the AI infrastructure hub of Europe. They planned their energy systems well and the rest followed.

France holds a different card: nuclear energy as baseload power. While the United States debates whether to revive its nuclear industry and China builds reactors at a pace the West cannot match, France already generates over 70% of its electricity from nuclear, firm, dispatchable, carbon-free power that data centers prize highly. As AI inference workloads grow and demand shifts from training clusters that can tolerate interruption to real-time applications that cannot, the value of firm baseload power rises sharply.

The EU is also beginning to move institutionally. Through 2025-2026, the European Commission is establishing at least 15 AI Factories across member states, backed by 1.5 billion euros in combined national and EU funding, with a further 20 billion euros mobilized through InvestAI for up to five AI gigafactories. The explicit goal is to triple the region’s data center processing capacity within five to seven years.

Nicolas Colin frames the deeper logic through Carlota Perez’s theory of technological revolutions: each major paradigm, steam, steel, oil, computing, has a maturity phase where the winners are determined not by software or innovation alone but by control of physical infrastructure. We are entering that phase for AI. The question of who controls the energy is becoming as important as who controls the model.

Europe has often been described as having missed the software revolution. That may be true. But if AI is becoming an industrial system, won on energy, hardware, and infrastructure rather than algorithms, then Europe’s decades of investment in clean, stable, affordable electricity may prove to have been preparation for a race it did not know it was entering.

Conclusion: The grid is the new battleground

In the previous Horizon edition, I asked: who controls intelligence? This edition adds a layer beneath that answer.

Whoever controls the energy that runs the infrastructure controls the intelligence. And the geography of clean, affordable, reliable electricity is becoming one of the most consequential maps in geopolitics.

The US built the models. China is building the electrostate. The Nordics, quietly and without any particular intention to dominate, built exactly what the AI era needs most.

There is a line from the Aker CEO at the Stargate Norway announcement worth holding onto: “Norway has a proud history of turning clean, renewable energy into industrial value, powering global industries like aluminium and fertiliser. Today, artificial intelligence and advanced data operations represent the next wave of value creation.”

The question for Europe is not whether to play. It is whether it understands fast enough that it is already holding some of the best cards on the table.

Whoever controls the electrons controls the intelligence.

Idriss 🌞